A. Form 990 is an annual reporting return that certain federally tax-exempt organizations must file with the IRS. It provides information on the filing organization’s mission, programs, and finances.

- The most common error is forgetting or not knowing to file the IRS Form 990. Failing to complete the 990 for three consecutive years can result in losing 501(C)(3) status.

- Incomplete Schedule A, the section of the form that requires charities and certain types of charitable trusts to list the salaries and benefits awarded to top officials and to top-paid independent contractors. This part of the form also focuses on advocacy activity and contains additional questions not covered on the Form 990 itself.

- Failing to note primary exempt mission as required in the statement of program accomplishments.

- Arithmetic errors account for about 20% of all 990 tax returns.

- Not having the signature of any of the organization’s officers.

- Failure to attach required supporting schedules.

- Not listing the correct tax year.

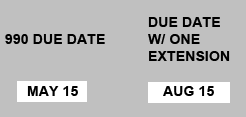

A. There is no one date on which all Forms 990 must be submitted to the IRS. Instead, a nonprofit’s filing date is determined by the end of its fiscal year (the 12-month period for which the organization plans the use of its funds). Each filing organization is required to file by the 15th day of the 5th month after its fiscal year ends. If your fiscal year ends on December 31, these are the filing dates:

A. Most federally tax-exempt organizations, with the exception of churches (unless there is unrelated business income) and state institutions. See the IRS guidelines.

A. IRS Publication 557 – Tax-Exempt Status for Your Organization, establishes an 85% of gross income requirement. This requirement is that the exempt organization must “. . . receive 85% or more of their gross income from their members for the sole purpose of meeting losses and expenses.” This 85% rule applies to ALL exempt organizations, not just 501(c)(4) social welfare organizations.

A. Yes. An exempt organization must establish an accounting system capable of tracking source of income and source of payment of that income. The system should also be able to identify those expenses directly connected to the production of income by source.

A. The tax rates are the same as those that apply to regular corporations on Form 1120. However, an exempt association files Form 990-T to report its unrelated business taxable income.

Most associations, simply by the nature of their operations, will not pay any significant income tax. This is because there is usually no net taxable income resulting from the unrelated business activities after allocation of expenses. Learm more about UBIT.